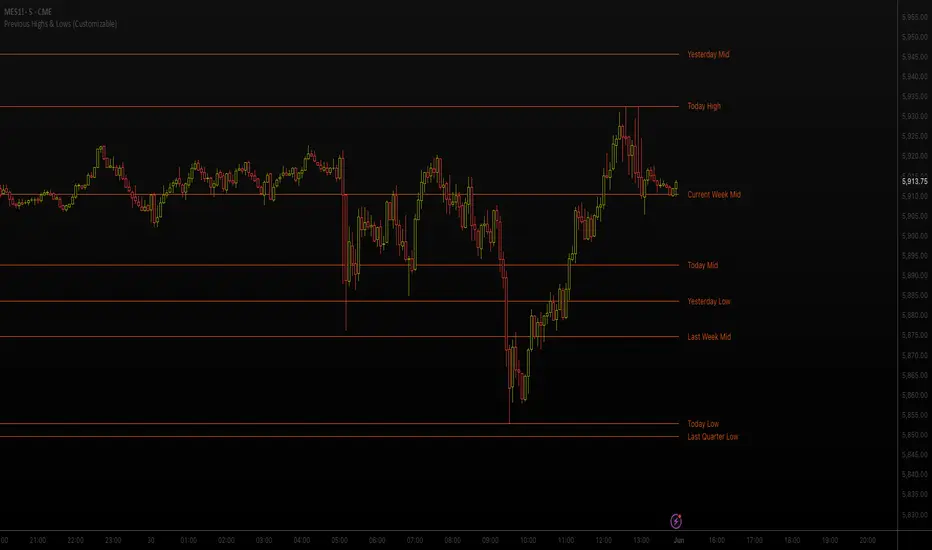

Previous Highs & Lows (Customizable)Previous Highs & Lows (Customizable)

This Pine Script indicator displays horizontal lines and labels for high, low, and midpoint levels across multiple timeframes. The indicator plots levels from the following periods:

Today's session high, low, and midpoint

Yesterday's high, low, and midpoint

Current week's high, low, and midpoint

Last week's high, low, and midpoint

Last month's high, low, and midpoint

Last quarter's high, low, and midpoint

Last year's high, low, and midpoint

Features

Individual Controls: Each timeframe has separate toggles for showing/hiding high/low levels and midpoint levels.

Custom Colors: Independent color selection for lines and labels for each timeframe group.

Display Options:

Adjustable line width (1-5 pixels)

Variable label text size (tiny, small, normal, large, huge)

Configurable label offset positioning

Organization: Settings are grouped by timeframe in a logical sequence from most recent (today) to least recent (last year).

Display Logic: Lines span the current trading day only. Labels are positioned to the right of the price action. The indicator automatically removes previous drawings to prevent chart clutter.

Search in scripts for "high low"

Inner Circle Toolkit [TakingProphets]Inner Circle Toolkit — A Complete ICT Trading Companion

The Inner Circle Toolkit is a closed-source, all-in-one trading tool designed for traders following ICT (Inner Circle Trader) and Smart Money Concepts strategies. Every part of this script is built with purpose — not just a mashup of indicators, but a structured framework to help you follow price through the lens of institutional behavior and liquidity theory.

Let’s walk through what it does and how it can help you:

🕒 Session Liquidity Levels (Asia, London, New York, NY Lunch)

The indicator automatically marks the highs and lows of the major trading sessions:

-Asian Session

-London Session

-New York AM Session

-New York Lunch

These levels are important because price often returns to these points to grab liquidity before making a move. This gives traders clear areas to watch for potential sweeps, rejections, or reversals — without having to manually track session timings every day.

REQHs and REQLs — Equal Highs and Lows

This script detects Relatively Equal Highs and Lows (REQHs/REQLs), which are often used by institutions as stop-run targets.

It’s not just looking for copy-paste double tops or bottoms — it uses a tolerance-based algorithm that checks for clusters of similar highs or lows over a given time period. These are likely to hold stops and become magnets for price. When you see these on the chart, you’ll know where the “juice” is sitting.

Fair Value Gaps (FVG) — Multi-Timeframe

The script automatically plots Fair Value Gaps (FVGs) on both:

-Your current chart timeframe

-One or more higher timeframes (like H1 or H4)

These are three-candle gaps that form when price moves aggressively without filling in value. Price often comes back to these areas to rebalance. Seeing both local and higher-timeframe FVGs on your chart gives better context and helps with entries and exits.

The script is optimized so your chart doesn’t get messy — higher timeframe FVGs show up in a cleaner format with visual labels and lighter shading.

SMT Divergence — With Session Logic

This tool includes a real-time SMT divergence detector, based on the behavior of correlated markets like ES vs. NQ.

Here’s how it works:

If ES sweeps a liquidity level (like Asia Low), but NQ doesn’t, the script detects and marks that divergence.

This often signals institutional accumulation or distribution — a high-probability setup.

You won’t have to flip between charts or manually compare — the SMT logic runs automatically and only fires when it matters (at key session levels). It’s a smarter, more focused way to track intermarket divergences.

Daily Highs and Lows — Week-to-Week Structure

The indicator keeps track of the high and low for each day of the week — Monday through Friday — helping you understand how price is evolving across the week.

This helps build a weekly profile:

Did Monday set the high of the week?

Are we sweeping Tuesday’s low on Thursday?

These levels stay visible and labeled, helping you frame daily setups inside the bigger picture.

🕛 Midnight Open & 8:30 AM Open Levels

These two levels are core ICT concepts used to judge whether price is in premium or discount:

Midnight Open (00:00 EST): Used to determine daily bias

New York Open (08:30 EST): Often a launch point for key moves

Both are drawn automatically and extend throughout the day. This helps you align your trades with potential algorithmic bias, especially during NY session volatility.

⏰ 9:45 AM Vertical Marker — Macro Time Reminder

The script draws a subtle vertical line at 9:45 AM EST, which is the start of the NY AM macro session — one of the most likely times to see setups play out.

This is more than just a timer — it’s a visual cue that something important might be setting up soon, especially if you’re already watching SMT, FVGs, or liquidity zones from earlier.

How It All Connects — A Workflow, Not a Mashup

Every feature in this script is connected to the same goal: helping you trade with the Smart Money.

Here’s how the pieces work together:

Session levels → potential stop hunts

Equal highs/lows → targets

FVGs → entry points

SMT divergence → confirmation or warning

Daily highs/lows → Weekly structure frames bias

Open levels → premium vs. discount

Macro line → timing clue for execution

It’s built to help you flow with price action and trade the story, not just random signals.

Why It’s Closed Source — and Original

This script is closed-source because it contains:

A proprietary system for real-time SMT logic (with intermarket sweep detection)

Multi-timeframe FVG detection that auto-filters overlaps

Smart equal-high/low detection using range-based clustering

Optimized UI that shows a lot without overwhelming the chart

There are no moving averages, no public-domain indicators, and no mashup of standard tools. Everything here is purpose-built for traders who follow ICT strategies.

Let us know how we can improve!

Advanced Market Structure & Order Blocks (fadi)Advanced Market Structure & Order Blocks indicator provides a new approach to understanding price action using ICT (Inner Circle Trader) concepts related to candle blocks to analyze the market behavior and eliminate much of the noise created by the price action.

This indicator is not intended to provide trade signals, it is designed to provide the traders with to support their trading strategies and add clarity where possible.

There are currently three main elements to this indicator:

Market Structure

Order Blocks

Liquidity Voids

Market Structure

In trading, market structure is often identified by observing higher highs and higher lows. An uptrend is characterized by a series of higher highs, where each peak surpasses the previous one, and higher lows, where each trough is higher than the preceding one. Conversely, a downtrend is marked by lower highs and lower lows.

Other indicators usually determine these peaks by calculating the highest or lowest levels within a predefined number of candles. For example, identifying the highest price level within the last 15 candles and marking it as a higher high or a lower high. While this approach offers some structure to price action, it can be arbitrary and random due to price fluctuations and the lack of proper structure analysis beyond finding the highest peaks and valleys within candle ranges.

In his 2022 mentorship, episode 12, ICT introduced an alternative approach focusing on three-candle pivots called Short Term High and Low (STH/STL), which are then used to calculate the Intermediate Term High and Low (ITH/ITL), and in turn, the Long Term High and Low (LTH/LTL). ICT’s approach provides better structure than the traditional method mentioned above. However, it can be confusing and difficult to track. There are great indicators that track and label ICT’s levels, but traders still find it challenging to follow and understand.

The Advanced Market Structure indicator takes a unique approach by analyzing candle formations, using ICT concepts, to identify possible turning points that mimic a real trader’s analysis of price action as closely as possible. However, it should be expected that Market Makers may use market manipulation to induce traders to make failed trades, and no tooling can eliminate these situations.

Advanced Market Structure tracks true Peaks and Valleys as they form, confirms them, and marks the chart with corresponding labels using traditional labeling methods (HH/HL/LH/LL), as such labeling makes it easier for traders to follow and understand. The indicator also draws levels to help identify possible liquidity areas and trade targets.

The indicator uses different calculation methods for the different type of market structure length, however all calculations are based on the same ICT candle blocks concepts.

Market Structure Settings

Other than the display settings, there are four (4) settings, mainly under the Level Settings section.

Allow Nested Candles

This option is only available on the Short Market Structure due to the methods used in calculating highs and lows. When used, the indicator will attempt to detect smaller fluctuations in price by tracking smaller candle moves, if any.

Level Settings

Level Settings allows the trader to decide two main calculations:

1. A new pivot point will form when a candle’s is crossed by the following candle’s

2. For a liquidity sweep and marking a level as mitigated, a candle’s must cross that level

Order Blocks

ICT (Inner Circle Trader) defines an Order Block as the last down-closing candle, or series of candles, before a significant upward price move or the last up-closing candle, or series of candles, before a significant downward price move. These key price levels, marked by substantial buy or sell orders from institutional traders or "smart money," create a block or zone on the price chart. When the price revisits these levels, it often leads to a strong market reaction. Order Blocks can consist of one or multiple consecutive candles of the same color, signaling areas of significant buying or selling interest. ICT's approach to Order Blocks provides traders with a structured method to identify potential areas of support or resistance, where price movements are more likely to change direction. Although ICT has shared some criteria for identifying Order Blocks publicly, the full details are reserved for his upcoming books. This indicator leverages the publicly available information to provide traders with valuable insights into these crucial price levels.

The Advanced Market Structure indicator is designed to be highly flexible, allowing traders to define their own combination of rules for identifying Order Blocks, thus customizing it to fit their unique trading strategies.

Order Block Configuration

Can be nested

An Order Block is defined as the last down candle or candles before a strong move higher, and vice versa for bearish Order Blocks. However, larger-than-usual candles resulting from news events or price action may not qualify as Order Blocks and can mute any Order Block within their range.

The "Can be nested" flag ensures that each Order Block is treated as an independent entity, even if it appears within the body of another Order Block.

Forms at swing point

Order Blocks formed at swing points typically have higher probabilities but are less frequent, assuming the same rules are applied. Additionally, Order Blocks at swing points may become Breaker and Mitigation blocks if they fail, providing more trading opportunities.

Forms a simple pivot point

A simple pivot point corresponds to ICT Short Term High and Low (STH/STL). Order Blocks using simple pivot points can occur in the middle of a move, not just at swing points. These are useful for identifying IOFED setups and supporting blocks that can bolster the price move.

Causes Market Structure Shift

Order Blocks that result in a break above or below a short swing point can help narrow down target order blocks, but they are less frequent. An Order Block causing a break above or below a pivot point does not necessarily indicate a strong Order Block. For example, an Order Block formed at a Lower Low is more likely to fail in a downtrend.

A clean close above order block

When the first candle breaks above an Order Block and closes above its high, this indicates a stronger Order Block. On the other hand, if a candle merely wicks through the Order Block without a solid close above it, it suggests a weaker Order Block. This may indicate hesitation or an impending reversal, as the wick represents a temporary and unsustained price movement.

Has displacement more than X the body

While some traders may capitalize on the initial break above an Order Block's CISD level, others prefer to focus on the return to an Order Block after displacement. Displacement is determined by the body size of the Order Block, and an Order Block cannot be tested until this level has been achieved.

Has a Fair Value Gap

When an Order Block is combined with a Fair Value Gap (FVG), it signifies a strong Order Block. The Fair Value Gap indicates a strong price movement away from the Order Block.

Has a liquidity void

A Liquidity Void occurs when two consecutive candles of the same color do not overlap, creating a gap similar to a Fair Value Gap, but involving one or more middle candles. Liquidity Voids can be utilized in combination with, or as an alternative to, the displacement setting.

Maximum number of OBs

The maximum number of Order Blocks to display.

Mitigated at block’s

An Order Block is considered mitigated when price reaches one of the main Order Block levels.

Liquidity Void

Liquidity Void refers to areas on a price chart where there is one-sided trading activity. This phenomenon occurs when the price of an asset moves sharply in one direction, leaving gaps where two consecutive candles of the same color do not overlap. These gaps can comprise one or more middle candles and indicates a pronounced lack of trading within that price range. Liquidity Voids are important because they highlight areas of minimal resistance, where price is more likely to return to fill the void and balance the market.

Liquidity Void vs Fair Value Gap

While both concepts are related to gaps in price action, they are distinct. A Fair Value Gap is a specific three-candle pattern where the middle candle creates a gap between the first and third candles. In contrast, a Liquidity Void represents a broader area on the chart where there is little to no trading activity, often encompassing multiple candles and indicating a more pronounced imbalance between buy and sell orders.

A FVG can be part of a Liquidity Void, a Liquidity Void can exist without necessarily including an FVG. Both concepts highlight areas of minimal resistance and potential price movement, but they differ in their formation and implications.

Advanced Market Structure and Order Blocks indicator focus on liquidity voids since a liquidity void can substitute for a FVG and it is usually less addressed by other indicators.

Morning RangeOverview

The Morning Range Indicator highlights the high and low of the market session from 6 AM to 10AM, providing key levels for potential breakout trades. The box dynamically updates in real-time, extending until 4 PM, and adjusts color based on price action.

This tool is ideal for traders looking to identify breakout opportunities and visualize key intraday price ranges.

How It Works

Session High & Low (6 AM - 10 AM)

The indicator tracks the highest high and lowest low within this time window.

Once 10 AM passes, the high and low are locked in and will not change.

Box Extends Until 4 PM

The session box remains visible throughout the trading day.

It provides a visual reference for potential breakout zones.

Dynamic Box Coloring

Gray (Neutral): Neither high nor low is broken.

Green: Only the high is broken before 4 PM.

Red: Only the low is broken before 4 PM.

Yellow: Both high and low are broken before 4 PM.

Live Updating Box

The box appears as soon as the session begins at 6 AM.

It dynamically updates the high and low until 10 AM.

Alerts for Breakouts

This indicator includes built-in alert conditions, so you can set up TradingView alerts without modifying the script.

Morning Range High Broken → Triggers when price breaks above the morning high.

Morning Range Low Broken → Triggers when price breaks below the morning low.

To set alerts:

Click the Alerts (⏰) icon in TradingView.

Select Condition → "Morning Range High Broken" or "Morning Range Low Broken".

Choose your preferred notification method (popup, email, webhook, etc.).

Click Create to activate the alert.

Who This Is For

✔ Intraday & Scalp Traders – Identify key breakout levels for short-term trades.

✔ Futures & Forex Traders – Works great for markets like NQ, ES, Gold, and FX pairs.

✔ Breakout & Reversal Traders – Use the high/low boundaries as support & resistance levels.

Customization

This indicator automatically updates every day and requires no manual input.

You can change alert settings via TradingView’s built-in alert system.

How to Use This Indicator

Watch for breakouts above/below the morning range as potential trade opportunities.

Combine with volume, momentum indicators, or footprint charts for confirmation.

Use the box color to visually assess whether price action is bullish (green), bearish (red), or ranging (gray).

Swing Breakout System (SBS)The Swing Breakout Sequence (SBS) is a trading strategy that focuses on identifying high-probability entry points based on a specific pattern of price swings. This indicator will identify these patterns, then draw lines and labels to show confirmation.

How To Use:

The indicator will show both Bullish and Bearish SBS patterns.

Bullish Pattern is made up of 6 points: Low (0), HH (1), LL (2 | but higher than initial Low), New HH (3), LL (5), LL again (5)

Bearish Patten is made up of 6 points: High (0), LL (1), HH (2 | but lower than initial high), New LL (3), HH (5), HH again (5)

A label with an arrow will appear at the end, showing the completion of a successful sequence

Idea behind the strategy:

The idea behind this strategy, is the accumulation and then manipulation of liquidity throughout the sequence. For example, during SBS sequence, liquidity is accumulated during step (2), then price will push away to make a new high/low (step 3), after making a minor new high/low, price will retrace breaking the key level set up in step (2). This is price manipulating taking liquidity from behind high/low from step (2). After taking liquidity price the idea is price will continue in the original direction.

Step 0 - Setting up initial direction

Step 1 - Setting up initial direction

Step 2 - Key low/high establishing liquidity

Step 3 - Failed New high/low

Step 4 - Taking liquidity from step (2)

Step 5 - Taking liquidity from step 2 and 4

Pattern Detection:

- Uses pivot high/low points to identify swing patterns

- Stores 6 consecutive swing points in arrays

- Identifies two types of patterns:

1. Bullish Pattern: A specific sequence of higher lows and higher highs

2. Bearish Pattern: A specific sequence of lower highs and lower lows

Note: Because the indicator is identifying a perfect sequence of 6 steps, set ups may not appear frequently.

Visualization:

- Draws connecting lines between swing points

- Labels each point numerically (optional)

- Shows breakout arrows (↑ for bullish, ↓ for bearish)

- Generates alerts on valid breakouts

User Input Settings:

Core Parameters

1. Pivot Lookback Period (default: 2)

- Controls how many bars to look back/forward for pivot point detection

- Higher values create fewer but more significant pivot points

2. Minimum Pattern Height % (default: 0.1)

- Minimum required height of the pattern as a percentage of price

- Filters out insignificant patterns

3. Maximum Pattern Width (bars) (default: 50)

- Maximum allowed width of the pattern in bars

- Helps exclude patterns that form over too long a period

Weekly Opening Range and Previous Data for FuturesThis indicator will not predict future price action.

This indicator is a time based range tool. These types of tools are great to use when there is not any historical data to look back on (as in all time highs/lows). The user can use this indicator to measure distributions, use deviations of the range to identify support/resistance levels, and see how historical price action influences current price action. This indicator is unique because it uses the price range from the open of the futures market on Sunday 18:00 America/New York to the open of the Bond Market 8:00 America/New York as the range for all calculations.

This indicator collects the multiple points of data from each day of the week, and gives the user many options on how to use the data that is collected. The amount of data collected is based on the time frame of the chart (best used on a 15 minute chart), but is limited to 30 minute charts.

Data Collected:

Opening Range for the week

High of Each Day

Low of Each Day

Close of Each Day

Initially the range is plotted on the chart as a box, when the Bond market opens the high/low/mid is plotted, as well as the current week open and previous week close.

How the data is used.

Intraday: Monday does not have a previous day to pull data on, so all data for Monday is intraday data. When a new high is made, the indicator will search all previous data in the lookback period for the current day , find all highs that are within a set variance (determined by the user), and plot the corresponding lows from the matching days. It will do the same for new lows that are made, with corresponding historical highs. All of these levels are plotted on the chart, as well as the Average High, Average Low. If price moves beyond either Average, the Average of all days that distributed higher than the Average is plotted on the chart as Min/Max Average.

Previous Day Data: Tuesday - Friday. After the close of the day, the user has the option to choose either the High, Low, or Close of that day to find previous data that matches within a variance determined by the user; or an option to find the n closest matches (up to 20). That data is then matched to the corresponding next day data and plotted on the chart as a box. Example: Monday closes at +1 Deviation (Dev) of the Weekly Opening Range (WOR). The user sets the variance at 0.5 (0.5 Dev of the WOR), the indicator will search the lookback period for all Mondays that closed between 1.25 Dev and 0.75 Dev of the WOR. The matching Mondays will then be matched to their corresponding Tuesdays and the data for the High and Low from those Tuesdays will be placed on the chart as a box overlaying the current Tuesday. Each match is numbered so that corresponding Highs and Lows of each historical day can be identified. The same can be done for either the High or Low of the Previous Day.

The indicator has a table that can be shown.

Data shown in table:

Current Extension of the WOR

Maximum Extension of the WOR

Average WOR in %

Current WOR in %

Average Range for the day in % based on data set

Current Range for the day in %

Number of days in the data set

Number of Previous Day Matches

Variance for previous day data

Number of Intraday High Matches

Number of Intraday Low Matches

Variance for Intraday Matches

The table as well as all lines and boxes have the option of being shown or not, as well as have their settings customized to fit the users chart layout.

As with any indicator, do not let the data shown change your trading model. Past performance is not indicative to future performance.

UVR Crypto TrendINDICATOR OVERVIEW: UVR CRYPTO TREND

The UVR Crypto Trend indicator is a custom-built tool designed specifically for cryptocurrency markets, utilizing advanced volatility, momentum, and trend-following techniques. It aims to identify trend reversals and provide buy and sell signals by analyzing multiple factors, such as price volatility(UVR), RSI (Relative Strength Index), CMF (Chaikin Money Flow), and EMA (Exponential Moving Average). The indicator is optimized for CRYPTO MARKETS only.

KEY FEATURES AND HOW IT WORKS

Volatility Analysis with UVR

The UVR (Ultimate Volatility Rate) is a proprietary calculation that measures market volatility by comparing significant price extremes and smoothing the data over time.

Purpose: UVR aims to reduce noise in low-volatility environments and highlight significant movements during higher-volatility periods. While it strives to improve filtering in low-volatility conditions, it does not guarantee perfect performance, making it a balanced and adaptable tool for dynamic markets like cryptocurrency.

HOW UVR (ULTIMATE VOLATILITY RATE) IS CALCULATED

UVR is calculated using a method that ensures precise measurement of market volatility by comparing price extremes across consecutive candles:

Volatility Components:

Two values are calculated to represent potential price fluctuations:

The absolute difference between the current candle's high and the previous candle's low:

Volatility Component 1=∣High−Low ∣

The absolute difference between the previous candle's high and the current candle's low:

Volatility Component 2=∣High −Low∣

Volatility Ratio:

The larger of the two components is selected as the Volatility Ratio, ensuring UVR captures the most significant movement:

Volatility Ratio=max(Volatility Component 1,Volatility Component 2)

Smoothing with SMMA:

To stabilize the volatility calculation, the Volatility Ratio is smoothed using a Smoothed Moving Average (SMMA) over a user-defined period (e.g., 14 candles):

UVR=(UVR(Previous)×(Period−1)+Volatility Ratio)/Period

This calculation ensures UVR adapts dynamically to market conditions, focusing on significant price movements while filtering out noise.

RSI FOR MOMENTUM DETECTION

RSI (Relative Strength Index) identifies overbought and oversold conditions.

Trend Confirmation at the 50 Level

RSI values crossing above 50 signal the potential start of an upward trend.

RSI values crossing below 50 indicate the potential start of a downward trend.

Key Reversals at Extreme Levels

RSI detects trend reversals at overbought (>70) and oversold (<30) levels.

For example:

Overbought Trend Reversal: RSI >70 followed by bearish price action signals a potential downtrend.

Oversold Trend Reversal: RSI <30 with bullish confirmation signals a potential uptrend.

Rare Extreme RSI Readings

Extreme levels, such as RSI <12 (oversold) or RSI >88 (overbought), are used to identify rare yet powerful reversals.

---HOW IT DIFFERS FROM OTHER INDICATORS---

Using UVR High and Low Values

The Ultimate Volatility Rate (UVR) focuses on analyzing the high and low price ranges of the market to measure volatility.

Unlike traditional trend indicators that rely primarily on momentum or moving average crossovers, UVR leverages price extremes to better identify trend reversals.

This approach ensures fewer false signals during low-volatility phases and more accurate trend detection during high-volatility conditions.

UVR as the Core Component

The indicator is fundamentally built around UVR as the primary filter, while supporting tools like RSI (momentum detection), CMF (volume confirmation), and EMA (trend validation) complement its functionality.

By integrating these additional components, the indicator provides a multidimensional analysis rather than relying solely on a single approach.

Dynamic Adaptation to Volatility

UVR dynamically adjusts to market conditions, striving to improve filtering in low-volatility phases. While not flawless, this approach minimizes false signals and adapts more effectively to varying levels of market activity.

Trend Clouds for Visual Guidance

UVR-based dynamic clouds visually mark high and low price areas, highlighting potential consolidation or retracement zones.

These clouds serve as guides for setting stop-loss or take-profit levels, offering clear risk management strategies.

BUY AND SELL SIGNAL LOGIC

BUY CONDITIONS

Momentum-Based Buy-Entry

RSI >50, CMF >0, and the close price is above EMA50.

The price difference between open and close exceeds a threshold based on UVR.

Oversold Reversal

RSI <30 and CMF >0 with a strong bullish candle (close > open and UVR-based sensitivity filter).

Breakout Confirmation

The price breaks above a previously identified resistance, with conditions for RSI and CMF supporting the breakout.

Reversal from Oversold RSI Extreme

RSI <12 on the previous candle with a strong rebound on the current candle with UVR confirmation filter.

SELL CONDITIONS

Momentum-Based Sell-Entry

RSI <50, CMF <0, and the close price is below EMA50.

The price difference between open and close exceeds the UVR threshold.

Overbought Reversal

RSI >70 with bearish price action (open > close and UVR-based sensitivity filter).

Breakdown Confirmation

The price breaks below a previously identified support, with RSI and CMF supporting the breakdown.

Reversal from Overbought RSI Extreme

RSI >88 on the previous candle with a bearish confirmation on the current candle with UVR confirmation filter.

BUY AND SELL SIGNALS VISUALIZATION

The UVR Crypto Trend Indicator visually represents buy and sell conditions using dynamic plots, making it easier for traders to interpret and act on the signals. Below is an explanation of the visual representation:

Buy Signals and Visualization

Signal Trigger:

A buy signal is generated when one of the defined Buy Conditions is met (e.g., RSI >50, CMF >0, price above EMA50).

Visual Representation:

A blue upward arrow appears at the candle where the buy condition is triggered.

A blue cloud forms above the price candles, representing the strength of the bullish trend. The cloud dynamically adapts to market volatility, using the UVR calculation to mark support zones or consolidation levels.

Purpose of the Blue Cloud:

It acts as a visual guide for price movements and stay horizontal when the trend is not moving up

Sell Signals and Visualization

Signal Trigger:

A sell signal is generated when one of the defined Sell Conditions is met (e.g., RSI <50, CMF <0, price below EMA50).

Visual Representation:

A red downward arrow appears at the candle where the sell condition is triggered.

A red cloud forms below the price candles, representing the strength of the bearish trend. Like the blue cloud, it uses the UVR calculation to dynamically mark resistance zones or potential retracement levels.

Purpose of the Red Cloud:

It acts as a visual guide for price movements and stay horizontal when the trend is not moving down.

CONCLUSION

The UVR Crypto Trend indicator provides a powerful tool for trend reversal detection by combining volatility analysis, momentum confirmation, and trend-following techniques. Its unique use of the Ultimate Volatility Rate (UVR) as a core element, supported by proven indicators like RSI, CMF, and EMA, ensures reliable and actionable signals tailored for the crypto market's dynamic nature. By leveraging UVR’s high and low price range analysis, it achieves a level of precision that traditional indicators lack, making it a high-performing system for cryptocurrency traders.

First 15-Min Candle Detector [With Breakout Alerts]Indicator: First 15-Minute Candle Detector

Purpose

This indicator helps traders by identifying and marking the high, low, and mid-point of the first 15-minute candle of the market session. It also provides visual aids and alerts for price breakouts above or below these levels, making it ideal for intraday trading strategies.

This script is suitable for traders focusing on early session momentum or reversal strategies.

Key Features

Market Start Customization: Configure the market start time (hour and minute) to align with your trading session or exchange timezone.

Visual Aids:

Horizontal lines to mark the High , Low , and Mid-point of the first 15-minute candle.

Background highlighting to identify the first 15-minute candle.

Configurable colors and line widths for clear visuals.

Breakout Alerts:

Real-time alerts for breakouts above the high or below the low of the first 15-minute candle.

Customizable alert messages.

Alerts configured using alertcondition .

Dynamic Adjustments:

Adapts dynamically to timeframes of 15 minutes or lower.

Resets and recalculates at the start of each new session.

Inputs and Configurations

Market Settings:

Market Start Hour: Default is 9.

Market Start Minute: Default is 30.

Visual Settings:

Enable/disable background highlighting.

Set colors for the background, high line, low line, and mid-line.

Adjust line width (1 to 5).

Toggle the visibility of the mid-line.

Alert Settings:

Enable breakout alerts.

Set custom alert messages for high and low breakouts.

How It Works

// First 15-Minute Candle Detection

The indicator monitors the first 15-minute candle after the market opens based on the configured start time. It records the high , low , and calculates the mid-point of this candle.

// Visual Markings

Horizontal lines are drawn at the high, low, and mid-point of the first 15-minute candle, extending to the right for the rest of the session.

// Breakout Detection

The indicator checks for price breakouts above the high or below the low of the first 15-minute candle and triggers alerts if enabled.

// Dynamic Reset

The indicator resets values and deletes previous session lines at the start of each new session.

Conditions and Alerts

Breakout Conditions:

High Breakout: The closing price exceeds the high of the first 15-minute candle.

Low Breakout: The closing price falls below the low of the first 15-minute candle.

Alert Triggers: Configurable alerts notify you of breakouts in real-time.

Use Cases

Intraday Traders: Ideal for early-session momentum or reversal strategies.

Breakout Traders: Helps identify entry points when price breaks key levels.

Visual Clarity: Simplifies tracking important session levels.

Limitations

Works only on 15-minute or lower timeframes.

Requires accurate market start time configuration.

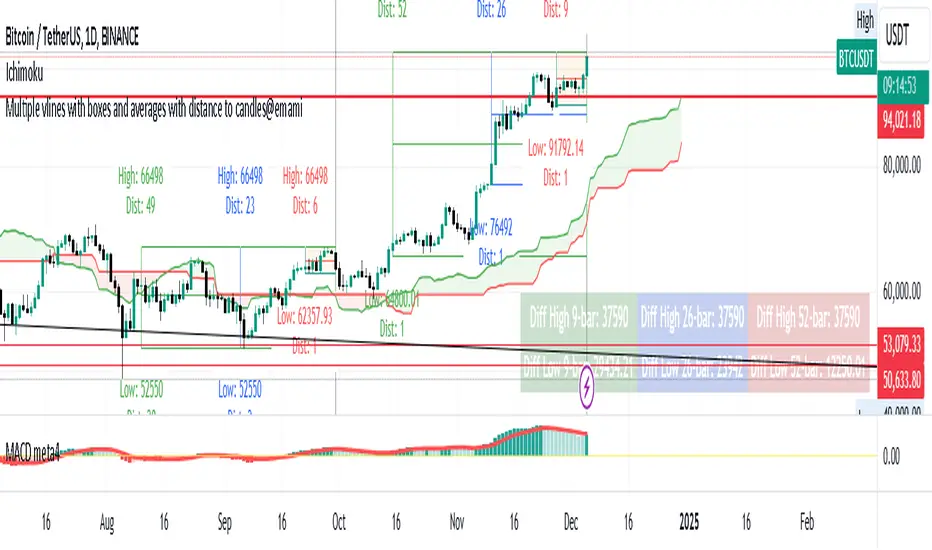

Multiple vlines boxes and averages distance to candles@emami

Indicator: "Multiple Vertical Lines with Boxes and Averages with Distance to Candles"

Description:

This Pine Script is designed to help traders analyze price movements over different time frames by visually drawing vertical lines and boxes based on selected date/time points. The script calculates the highest high, lowest low, and midpoints of the last 9, 26, and 52 bars, drawing a box around each range. Additionally, the script displays the distance from the high and low to the current bar.

Key Features:

Multiple Vertical Lines:

Vertical lines are drawn at user-specified times, allowing traders to highlight critical points on the chart for further analysis.

Dynamic Boxes Based on Bar Count:

9-bar Box: Displays the highest high and lowest low for the last 9 bars (including the current bar) and draws a box around this range. A midpoint line is also plotted.

26-bar Box: Similar to the 9-bar box, but for the last 26 bars.

52-bar Box: Displays the same calculation for the last 52 bars.

Distance Calculations:

The script calculates the distance from the highest high and lowest low of each box to the current bar, providing valuable insight into the range and price movement for each time window.

Visual Display:

Each box is colored differently for easy identification (orange for 9 bars, white for 26 bars, and green for 52 bars).

Midpoint lines are drawn in different colors to distinguish between the 9-bar, 26-bar, and 52-bar ranges.

Labels are placed above the high and below the low of each box, showing the exact high/low values and the distance to the current bar.

How It Works:

The script first waits for the specified date and time inputs. Once the time condition is met, it performs the calculations for the high, low, and midpoint of the last 9, 26, and 52 bars.

The script then plots vertical lines at the specified times and draws boxes based on the highest high and lowest low for each range.

A midpoint is drawn for each box, and labels are placed with the high/low values and the distances from these values to the current bar.

How to Use It:

Set the date and time for the vertical lines you want to analyze.

The script will automatically draw the lines and boxes for the selected time frames.

Review the boxes and midpoints to identify potential price levels for analysis.

Use the distance values to assess the current price's proximity to the high/low of the respective bar range.

Improvements Based on Rules:

Language:

Make sure your title and description are in English. If you use any other language, ensure it’s accompanied by an English translation.

Clean Chart:

Ensure that the chart you’re publishing with the script is clear and simple, without additional, unnecessary indicators or drawings.

Originality & Usefulness:

If your script is closed-source, clarify why it is closed-source. Provide enough details about its unique functionality so traders can understand its purpose and utility.

No Advertisements or Promotions:

Double-check that your description does not contain any links, promotional content, or references to websites, companies, or social media.

Suggested Tags for Script:

#PineScript

#VerticalLines

#PriceAnalysis

#TechnicalAnalysis

#SupportResistance

#BoxingStrategy

#MidpointCalculation

#DistanceToCandles

#ChartIndicators

BOS TRADER [v 1.0] [Influxum]The name of the tool, BOS Trader, comes from the abbreviation BOS, which stands for Break Of Structure. In simple terms, this tool identifies situations where a change in market structure occurs after liquidity has been grabbed. Following the structural change, it looks for a point where the balance between buyers and sellers will be tested, potentially continuing the price movement in the direction of the structural break.

The goal of this tool is to identify areas where a trader can look for potential entry opportunities based on their entry rules and filters. In our own research, we found that while this tool is not a standalone strategy, it provides a statistical advantage that stems from the nature of the market itself. If you expect the market to reverse at a certain price level against a short-term, medium-term, or long-term trend, that reversal must logically begin with a change in structure – i.e., its break. BOS Trader then highlights the zone where you can expect a strong reaction from traders speculating on the continuation of price in the direction of the break.

Another important piece of the puzzle is the concept of liquidity. Liquidity grabs are generally considered by traders to be events that can trigger market direction changes. That's why BOS Trader is complemented with multiple ways to identify liquidity in the market from a Price Action perspective. We have explored the liquidity concept in depth in our other tools – the Liquidity Tool and Liquidity Strategy Tester – so we won’t go into too much detail on liquidity settings here.

🟪 Pivots

Liquidity can be found beyond pivot extremes – the highest candles in a series of candles. The pivot liquidity setting specifies how many candles must be before and after the pivot candle with a lower high for a pivot high or a higher low for a pivot low. A pivot high is the local highest point of the last 31 candles (15 before the pivot candle, the pivot candle itself, and 15 after). Another option is to set the time period in which the pivot extreme must occur. For example, you can differentiate between pivot highs of the Asian or London session.

🟪 % Percent Change

This setting is based on the well-known Zig Zag indicator and confirms swing highs or swing lows when there is a certain percentage change in price. This helps filter out noise that can occur when the market consolidates and randomly creates pivot highs or lows that aren’t significant.

🟪 Session High/Low

Many popular strategies are based on liquidity defined as the price range of a specific trading session. This doesn't have to be London, Asia, or New York sessions, but could be, for instance, the first hour of the New York session, and so on.

🟪 Day High/Low, Week High/Low, Month High/Low

As the name suggests, liquidity is often defined by the high/low of the previous day, week, or month. These price levels are watched by many market participants, and it's reasonable to expect reactions at these levels. That’s why we included this option in the BOS tool.

Tip for Traders

To avoid common issues with setting the correct session time, we have added the BG option to the tool – the ability to display a background for the configured trading session. This makes it easy to verify that your trading session is set correctly in relation to your time zone.

Delete grabbed liquidity

If a liquidity level is breached by price, it becomes invalid. For those who prefer to keep their charts clean and uncluttered, there is an option to delete grabbed liquidity. This way, only untraded, valid liquidity lines will be visible on the chart.

Bars after liquidity grab

A liquidity grab should be a significant event that triggers a reaction from market participants. To ensure this is a real response to liquidity rather than random market behavior, we added a time test to the BOS tool. A structural break must occur within a specified time after the liquidity grab. You can define this time in the tool as the number of bars after which the structural break is still considered valid following the liquidity grab.

🟪 AOI (Area of Interest) Settings

Initially, it's important to note that there are two main options for setting the behavior of the AOI. The first option is to fix its duration by the number of bars – Duration, and the second is to keep the AOI valid until it is traded through – Extended.

Duration

Since we expect a quick reaction to the liquidity grab, we also expect a fast pullback to the AOI and a swift response of traders. Our research has shown that the strongest reactions typically occur within a maximum of 15 bars from the formation of the AOI (fractally across timeframes). Therefore, this value is set as the default. However, we recommend considering not just the speed of the reaction but also its intensity. After the set number of bars, the AOI stops extending further.

Extended

We have noticed that price has a tendency to return to the AOI even after a longer period and react again. For this reason, we included the option in the BOS tool to extend the AOI into the future, with the ability to freely adjust the Max AOI Length.

🟪 AOI Size Mode

There are two options for setting the size of the AOI. Either it can be calculated as a percentage of the swing size (% of swing) in which the structural break occurred (the default setting is 30%), or you can set a different concept for the AOI size. For example, the well-known Optimal Trade Entry model. Custom values can be set in the FIBO Levels option, where you can define either preferred Fibonacci values or values based on your own criteria.

🟪 Trading Session (signals + alerts + visibility)

The main goal of our tools is to make it easier for traders to identify patterns and opportunities in the market and allow them to be alerted to their occurrence. The time for AOI plotting after a liquidity grab is combined into a single Trading Session function. This controls both the AOI plotting and when the tool will send alerts. All of this is aimed at helping traders avoid spending the entire day in front of their monitors, waiting for trading opportunities. Here, too, you can use the BG feature to plot a background on the chart showing the current session.

🟪 Trading within session range

We found that some traders have difficulty navigating the many AOIs plotted during times when the market consolidates and creates numerous false breakouts. Therefore, we included an option in the BOS tool to track only structural changes at the price extremes of the current day and trading session. The tool will not plot structural changes for internal liquidity grabs (within the session range), but only for external liquidity grabs (highest highs and lowest lows of the session or liquidity from previous days).

Visuals

The BOS tool is, of course, supplemented with the option to customize the appearance of all its components according to your preferences.

Enhanced MACD Swing Analysis增強版 MACD 擺動分析

概述

增強版 MACD 擺動分析是一個適用於 TradingView 的技術指標,它通過額外的視覺工具增強了傳統的 MACD(移動平均收斂背離),以幫助識別擺動高點和低點。該指標旨在幫助交易者可視化動能的變化,並更準確地確定市場進出位置。它提供基於可自定義閾值的動態顏色變化直方圖,並直接在圖表上繪製擺動高/低點的線條,方便分析。

功能

MACD 計算:該腳本包括傳統的 MACD 計算,並且允許調整快速長度、慢速長度和信號平滑參數。

擺動高/低點檢測:根據用戶定義的回看週期,自動檢測擺動高點和低點,並在圖表右上角顯示這些數值。

動態顏色變化直方圖:根據 MACD 比率動態改變直方圖的顏色,使交易者可以輕鬆識別不同的動能強度。顏色可以自定義,正負動能都有多種色調。

擺動高/低點線條:繪製線條以視覺化顯示擺動高點和低點,並向右延伸這些線條,以便更好地視覺指引。

參數

快速長度 (MACD Fast Length):計算快速移動平均的週期數。預設值為 12。

慢速長度 (MACD Slow Length):計算慢速移動平均的週期數。預設值為 26。

信號平滑 (MACD Signal Smoothing):平滑 MACD 信號線的週期數。預設值為 9。

擺動回看範圍 (Swing Lookback Range):回看多少根 K 線以檢測擺動高點和低點。預設值為 25。

顏色變化比率 (Color Change Ratios):逗號分隔的比率,用於定義直方圖顏色變化的閾值。這些閾值允許用戶自定義何時基於 MACD 比率改變直方圖的顏色強度。提供了默認值。

工作原理

MACD 計算:該腳本使用用戶定義的快速和慢速長度,以及信號線平滑來計算 MACD。

直方圖顏色變化:根據 MACD 線和信號線之間的差值,計算比率以確定直方圖顏色的強度。顏色根據用戶指定的閾值進行變化,以視覺化顯示動能的變化。

擺動高/低點檢測:腳本回看一定數量的 K 線來檢測擺動高點和低點,並在圖表上繪製向右延伸的線條,方便識別。

使用方法

添加到圖表:將指標應用到您的 TradingView 圖表上,以更清晰地可視化 MACD 動能。

調整參數:根據您的交易風格自定義參數。您可以調整 MACD 長度、擺動回看範圍和顏色變化閾值。

解讀信號:使用顏色編碼的直方圖來判斷動能的強弱和方向。擺動高/低點線條有助於識別潛在的市場反轉或進出場位置。

實際應用

動能分析:使用顏色變化直方圖來評估趨勢的強度。顏色越亮表示動能越強,顏色越暗表示趨勢減弱。

擺動識別:擺動高/低點線條便於識別價格可能反轉的支撐和阻力區域。

進出場信號:當直方圖顏色強度變化時,這可能是動能轉變的早期信號,提供潛在的買入或賣出機會。

自定義

該指標高度可自定義,允許交易者修改 MACD 參數、擺動回看範圍和顏色變化閾值。這種靈活性使其適合於不同的交易風格,無論是日內交易者、擺動交易者,還是長期投資者。

Enhanced MACD Swing Analysis

Overview

The Enhanced MACD Swing Analysis script is a technical indicator for TradingView that enhances the traditional MACD (Moving Average Convergence Divergence) with additional visual tools to identify swing highs and swing lows. This indicator is designed to help traders visualize momentum shifts and determine market entry/exit points with greater accuracy. It provides dynamic color-changing histograms based on customizable thresholds and draws swing high/low lines directly on the chart for easy analysis.

Features

MACD Calculation: The script includes the traditional MACD calculation, with adjustable parameters for fast length, slow length, and signal smoothing.

Swing High/Low Detection: Automatically detects swing highs and lows based on a user-defined lookback period and displays the values in the top-right corner of the chart.

Dynamic Color-Changing Histogram: The histogram colors change dynamically based on the MACD ratio, allowing traders to easily identify different levels of momentum. The colors are customizable, with a variety of shades for both positive and negative momentum.

Swing High/Low Lines: Draws lines to visually indicate swing highs and lows, extending these lines to the right for better visual guidance.

Parameters

快速長度 (MACD Fast Length): The number of periods for the fast moving average. Default is 12.

慢速長度 (MACD Slow Length): The number of periods for the slow moving average. Default is 26.

信號平滑 (MACD Signal Smoothing): The number of periods for smoothing the MACD signal line. Default is 9.

擺動回看範圍 (Swing Lookback Range): The number of bars to look back for detecting swing highs and lows. Default is 25.

顏色變化比率 (Color Change Ratios): Comma-separated values for defining the ratios at which histogram colors change. These thresholds allow users to customize when the histogram changes its color intensity based on the MACD ratio. Default values are provided.

How It Works

MACD Calculation: The script calculates the MACD using the user-defined fast and slow lengths, along with a signal line for smoothing.

Histogram Color Change: Based on the difference between the MACD line and the signal line, a ratio is calculated to determine the intensity of the histogram's color. The color changes depending on user-specified thresholds to visually indicate shifts in momentum.

Swing High/Low Detection: The script looks back over a specified number of bars to detect swing highs and lows, which are then plotted on the chart using lines that extend to the right for easier identification.

How to Use

Add to Chart: Apply the indicator to your TradingView chart to visualize MACD momentum with enhanced clarity.

Adjust Parameters: Customize the parameters to suit your trading style. You can adjust the MACD lengths, swing lookback range, and color change thresholds as needed.

Interpret the Signals: Use the color-coded histogram to gauge momentum strength and direction. The swing high/low lines help identify key levels for potential market reversals or entry/exit points.

Practical Applications

Momentum Analysis: Use the color-changing histogram to assess the strength of a trend. Brighter colors indicate stronger momentum, while darker colors suggest weakening trends.

Swing Identification: The swing high and low lines make it easy to identify support and resistance areas where price may reverse.

Entry and Exit Signals: When the histogram color intensity changes, it could be an early indication of a shift in momentum, providing potential buy or sell opportunities.

Customization

This indicator is highly customizable, allowing traders to modify the MACD parameters, swing lookback range, and color change thresholds. This flexibility makes it suitable for different trading styles, whether you're a day trader, swing trader, or long-term investor.

Time and Price Lines and Zones (fadi)

Draw a red line starting from the open at 9:30

Show dotted lines between 11 and 12 and shade it

Mark the ORB high and low from 9:30 to 10:00 and extend it in orange and shade it

In trading, time and price are two crucial elements that help traders make decisions about buying and selling assets like stocks, commodities, or currencies. Forex or futures traders may prefer to trade during the Asia, London, and New York sessions to increase the probability of price moves. Additionally, traders often focus on key levels on the chart to frame their trades.

The Time and Price Lines and Zones indicator allows traders to set an unlimited number of time- and price-based levels on a chart, with full control over how they are displayed. Traders can simply type in their desired settings, and the indicator will interpret the instructions and plot the levels on the chart.

However, as it is a scripted tool, there are some limitations, and traders should keep their inputs relatively straightforward.

How It Works

In the settings, you type in the time and price levels you'd like to see, along with the timeframes for display. Each new line will render a line, a set of lines, or a price zone within a specific time interval. You can specify starting and ending times, price levels such as highs and lows, and details like color, line style, and thickness.

The following are some settings you can use:

Time

Always required, formatted as 0 to 23 for hours (with 0 representing midnight) and 0 to 59 for minutes. You can specify just a start time or both start and end times to "box" a period.

Examples:

1 ( for 1:00 AM)

13 (for 1:00 PM)

13:50 (for 1:50 PM)

Price

Optional. If no price level is provided, the indicator will treat it as an open time window and draw vertical lines at the specified time intervals.

Color

The indicator recognizes the 17 built-in colors from TradingView ( www.tradingview.com ). You also have the option to override or create your own colors to match your color schema under settings. Silver (light gray) is the default if none is specified.

Line Style

There are three available line styles:

Solid (default)

Dashed

Dotted

Line Thickness

Line thickness can also be controlled with the following options:

Thin (default)

Medium

Thick

Fill or No Fill

When specifying two price levels, or two time periods, you can choose to keep the area between them empty or fill it with a semitransparent color. You can set this by specifying "shade," "shaded," "fill," or "filled."

Extend or Not

There are times, such as with the Open Range Breakout (ORB), where you may want to extend the zone without tracking additional price level changes. You can indicate this by specifying whether you want to extend it or not.

Additional Indicator Settings

Ignore lines that start with a defined character to instruct the indicator to ignore the line. For example, if you want to hide a line without deleting it, add # in front of it (default is #).

Hide Above Will hide all lines and zones above a defined timeframe.

Show Next Area Hours in Advance This will plot lines in advance to the right of the current price action, helping traders recognize upcoming points of interest.

Show Last X Days This controls the clutter on the screen by limiting the display to the most recent X number of days.

Fill Transparency The percentage of transparency applied to the background when a fill is specified.

Examples:

12 to 13 gray area shaded with dotted lines

Will result in two vertical lines, one at 12 noon and one at 1 PM, with the area between them shaded gray and a dotted line style.

0:00 vertical line red solid

Adds one vertical red line at midnight.

By specifying the open, high, low, and/or close price components, the indicator will interpret this as an instruction to draw a horizontal line at the specified price level. If two or more price levels are provided, each will be tracked accordingly.

Draw a red line starting from 0 open

Draws a line starting from midnight open until the end of the trading day.

Track high and low starting from 9:30 in a dashed green medium line

Tracks the day’s high and low, adjusting as new highs and lows are drawn in a dashed thicker green line from 9:30 AM until the end of trading hours.

# Asia

20 to 0 green high to low filled

# London

2:00 to 5 blue low and high filled

#New York

8:30 to 11:30 orange zone shaded orange between the high and low dotted

Adds three ICT Kill Zones for Asia, London, and New York based on their respective high and low.

8:30 to 11:30 orange zone shaded orange open close dotted

Will add a second New York zone overlapping the high and low zone.

#Draw Open Range Breakout (ORB)

9:30 to 10:00 purple extended zone

Extends the zone from 9:30 to 10:00 AM with a purple extended zone.

Multiple Naked LevelsPURPOSE OF THE INDICATOR

This indicator autogenerates and displays naked levels and gaps of multiple types collected into one simple and easy to use indicator.

VALUE PROPOSITION OF THE INDICATOR AND HOW IT IS ORIGINAL AND USEFUL

1) CONVENIENCE : The purpose of this indicator is to offer traders with one coherent and robust indicator providing useful, valuable, and often used levels - in one place.

2) CLUSTERS OF CONFLUENCES : With this indicator it is easy to identify levels and zones on the chart with multiple confluences increasing the likelihood of a potential reversal zone.

THE TYPES OF LEVELS AND GAPS INCLUDED IN THE INDICATOR

The types of levels include the following:

1) PIVOT levels (Daily/Weekly/Monthly) depicted in the chart as: dnPIV, wnPIV, mnPIV.

2) POC (Point of Control) levels (Daily/Weekly/Monthly) depicted in the chart as: dnPoC, wnPoC, mnPoC.

3) VAH/VAL STD 1 levels (Value Area High/Low with 1 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH1/dnVAL1, wnVAH1/wnVAL1, mnVAH1/mnVAL1

4) VAH/VAL STD 2 levels (Value Area High/Low with 2 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH2/dnVAL2, wnVAH2/wnVAL2, mnVAH1/mnVAL2

5) FAIR VALUE GAPS (Daily/Weekly/Monthly) depicted in the chart as: dnFVG, wnFVG, mnFVG.

6) CME GAPS (Daily) depicted in the chart as: dnCME.

7) EQUILIBRIUM levels (Daily/Weekly/Monthly) depicted in the chart as dnEQ, wnEQ, mnEQ.

HOW-TO ACTIVATE LEVEL TYPES AND TIMEFRAMES AND HOW-TO USE THE INDICATOR

You can simply choose which of the levels to be activated and displayed by clicking on the desired radio button in the settings menu.

You can locate the settings menu by clicking into the Object Tree window, left-click on the Multiple Naked Levels and select Settings.

You will then get a menu of different level types and timeframes. Click the checkboxes for the level types and timeframes that you want to display on the chart.

You can then go into the chart and check out which naked levels that have appeared. You can then use those levels as part of your technical analysis.

The levels displayed on the chart can serve as additional confluences or as part of your overall technical analysis and indicators.

In order to back-test the impact of the different naked levels you can also enable tapped levels to be depicted on the chart. Do this by toggling the 'Show tapped levels' checkbox.

Keep in mind however that Trading View can not shom more than 500 lines and text boxes so the indocator will not be able to give you the complete history back to the start for long duration assets.

In order to clean up the charts a little bit there are two additional settings that can be used in the Settings menu:

- Selecting the price range (%) from the current price to be included in the chart. The default is 25%. That means that all levels below or above 20% will not be displayed. You can set this level yourself from 0 up to 100%.

- Selecting the minimum gap size to include on the chart. The default is 1%. That means that all gaps/ranges below 1% in price difference will not be displayed on the chart. You can set the minimum gap size yourself.

BASIC DESCRIPTION OF THE INNER WORKINGS OF THE INDICTATOR

The way the indicator works is that it calculates and identifies all levels from the list of levels type and timeframes above. The indicator then adds this level to a list of untapped levels.

Then for each bar after, it checks if the level has been tapped. If the level has been tapped or a gap/range completely filled, this level is removed from the list so that the levels displayed in the end are only naked/untapped levels.

Below is a descrition of each of the level types and how it is caluclated (algorithm):

PIVOT

Daily, Weekly and Monthly levels in trading refer to significant price points that traders monitor within the context of a single trading day. These levels can provide insights into market behavior and help traders make informed decisions regarding entry and exit points.

Traders often use D/W/M levels to set entry and exit points for trades. For example, entering long positions near support (daily close) or selling near resistance (daily close).

Daily levels are used to set stop-loss orders. Placing stops just below the daily close for long positions or above the daily close for short positions can help manage risk.

The relationship between price movement and daily levels provides insights into market sentiment. For instance, if the price fails to break above the daily high, it may signify bearish sentiment, while a strong breakout can indicate bullish sentiment.

The way these levels are calculated in this indicator is based on finding pivots in the chart on D/W/M timeframe. The level is then set to previous D/W/M close = current D/W/M open.

In addition, when price is going up previous D/W/M open must be smaller than previous D/W/M close and current D/W/M close must be smaller than the current D/W/M open. When price is going down the opposite.

POINT OF CONTROL

The Point of Control (POC) is a key concept in volume profile analysis, which is commonly used in trading.

It represents the price level at which the highest volume of trading occurred during a specific period.

The POC is derived from the volume traded at various price levels over a defined time frame. In this indicator the timeframes are Daily, Weekly, and Montly.

It identifies the price level where the most trades took place, indicating strong interest and activity from traders at that price.

The POC often acts as a significant support or resistance level. If the price approaches the POC from above, it may act as a support level, while if approached from below, it can serve as a resistance level. Traders monitor the POC to gauge potential reversals or breakouts.

The way the POC is calculated in this indicator is by an approximation by analysing intrabars for the respective timeperiod (D/W/M), assigning the volume for each intrabar into the price-bins that the intrabar covers and finally identifying the bin with the highest aggregated volume.

The POC is the price in the middle of this bin.

The indicator uses a sample space for intrabars on the Daily timeframe of 15 minutes, 35 minutes for the Weekly timeframe, and 140 minutes for the Monthly timeframe.

The indicator has predefined the size of the bins to 0.2% of the price at the range low. That implies that the precision of the calulated POC og VAH/VAL is within 0.2%.

This reduction of precision is a tradeoff for performance and speed of the indicator.

This also implies that the bigger the difference from range high prices to range low prices the more bins the algorithm will iterate over. This is typically the case when calculating the monthly volume profile levels and especially high volatility assets such as alt coins.

Sometimes the number of iterations becomes too big for Trading View to handle. In these cases the bin size will be increased even more to reduce the number of iterations.

In such cases the bin size might increase by a factor of 2-3 decreasing the accuracy of the Volume Profile levels.

Anyway, since these Volume Profile levels are approximations and since precision is traded for performance the user should consider the Volume profile levels(POC, VAH, VAL) as zones rather than pin point accurate levels.

VALUE AREA HIGH/LOW STD1/STD2

The Value Area High (VAH) and Value Area Low (VAL) are important concepts in volume profile analysis, helping traders understand price levels where the majority of trading activity occurs for a given period.

The Value Area High/Low is the upper/lower boundary of the value area, representing the highest price level at which a certain percentage of the total trading volume occurred within a specified period.

The VAH/VAL indicates the price point above/below which the majority of trading activity is considered less valuable. It can serve as a potential resistance/support level, as prices above/below this level may experience selling/buying pressure from traders who view the price as overvalued/undervalued

In this indicator the timeframes are Daily, Weekly, and Monthly. This indicator provides two boundaries that can be selected in the menu.

The first boundary is 70% of the total volume (=1 standard deviation from mean). The second boundary is 95% of the total volume (=2 standard deviation from mean).

The way VAH/VAL is calculated is based on the same algorithm as for the POC.

However instead of identifying the bin with the highest volume, we start from range low and sum up the volume for each bin until the aggregated volume = 30%/70% for VAL1/VAH1 and aggregated volume = 5%/95% for VAL2/VAH2.

Then we simply set the VAL/VAH equal to the low of the respective bin.

FAIR VALUE GAPS

Fair Value Gaps (FVG) is a concept primarily used in technical analysis and price action trading, particularly within the context of futures and forex markets. They refer to areas on a price chart where there is a noticeable lack of trading activity, often highlighted by a significant price movement away from a previous level without trading occurring in between.

FVGs represent price levels where the market has moved significantly without any meaningful trading occurring. This can be seen as a "gap" on the price chart, where the price jumps from one level to another, often due to a rapid market reaction to news, events, or other factors.

These gaps typically appear when prices rise or fall quickly, creating a space on the chart where no transactions have taken place. For example, if a stock opens sharply higher and there are no trades at the prices in between the two levels, it creates a gap. The areas within these gaps can be areas of liquidity that the market may return to “fill” later on.

FVGs highlight inefficiencies in pricing and can indicate areas where the market may correct itself. When the market moves rapidly, it may leave behind price levels that traders eventually revisit to establish fair value.

Traders often watch for these gaps as potential reversal or continuation points. Many traders believe that price will eventually “fill” the gap, meaning it will return to those price levels, providing potential entry or exit points.

This indicator calculate FVGs on three different timeframes, Daily, Weekly and Montly.

In this indicator the FVGs are identified by looking for a three-candle pattern on a chart, signalling a discrete imbalance in order volume that prompts a quick price adjustment. These gaps reflect moments where the market sentiment strongly leans towards buying or selling yet lacks the opposite orders to maintain price stability.

The indicator sets the gap to the difference from the high of the first bar to the low of the third bar when price is moving up or from the low of the first bar to the high of the third bar when price is moving down.

CME GAPS (BTC only)

CME gaps refer to price discrepancies that can occur in charts for futures contracts traded on the Chicago Mercantile Exchange (CME). These gaps typically arise from the fact that many futures markets, including those on the CME, operate nearly 24 hours a day but may have significant price movements during periods when the market is closed.

CME gaps occur when there is a difference between the closing price of a futures contract on one trading day and the opening price on the following trading day. This difference can create a "gap" on the price chart.

Opening Gaps: These usually happen when the market opens significantly higher or lower than the previous day's close, often influenced by news, economic data releases, or other market events occurring during non-trading hours.

Gaps can result from reactions to major announcements or developments, such as earnings reports, geopolitical events, or changes in economic indicators, leading to rapid price movements.

The importance of CME Gaps in Trading is the potential for Filling Gaps: Many traders believe that prices often "fill" gaps, meaning that prices may return to the gap area to establish fair value.

This can create potential trading opportunities based on the expectation of gap filling. Gaps can act as significant support or resistance levels. Traders monitor these levels to identify potential reversal points in price action.

The way the gap is identified in this indicator is by checking if current open is higher than previous bar close when price is moving up or if current open is lower than previous day close when price is moving down.

EQUILIBRIUM

Equilibrium in finance and trading refers to a state where supply and demand in a market balance each other, resulting in stable prices. It is a key concept in various economic and trading contexts. Here’s a concise description:

Market Equilibrium occurs when the quantity of a good or service supplied equals the quantity demanded at a specific price level. At this point, there is no inherent pressure for the price to change, as buyers and sellers are in agreement.

Equilibrium Price is the price at which the market is in equilibrium. It reflects the point where the supply curve intersects the demand curve on a graph. At the equilibrium price, the market clears, meaning there are no surplus goods or shortages.

In this indicator the equilibrium level is calculated simply by finding the midpoint of the Daily, Weekly, and Montly candles respectively.

NOTES

1) Performance. The algorithms are quite resource intensive and the time it takes the indicator to calculate all the levels could be 5 seconds or more, depending on the number of bars in the chart and especially if Montly Volume Profile levels are selected (POC, VAH or VAL).

2) Levels displayed vs the selected chart timeframe. On a timeframe smaller than the daily TF - both Daily, Weekly, and Monthly levels will be displayed. On a timeframe bigger than the daily TF but smaller than the weekly TF - the Weekly and Monthly levels will be display but not the Daily levels. On a timeframe bigger than the weekly TF but smaller than the monthly TF - only the Monthly levels will be displayed. Not Daily and Weekly.

CREDITS

The core algorithm for calculating the POC levels is based on the indicator "Naked Intrabar POC" developed by rumpypumpydumpy (https:www.tradingview.com/u/rumpypumpydumpy/).

The "Naked intrabar POC" indicator calculates the POC on the current chart timeframe.

This indicator (Multiple Naked Levels) adds two new features:

1) It calculates the POC on three specific timeframes, the Daily, Weekly, and Monthly timeframes - not only the current chart timeframe.

2) It adds functionaly by calculating the VAL and VAH of the volume profile on the Daily, Weekly, Monthly timeframes .

Equal Highs and Lows {Reh's and Rel's }# Equal Highs and Lows {Reh's and Rel's} Indicator

## Overview

The "Equal Highs and Lows {Reh's and Rel's}" indicator is designed to identify and mark equal highs and lows on a price chart. It detects both exact and relative equal levels, draws lines connecting these levels, and optionally labels them. This tool can help traders identify potential support and resistance zones based on historical price levels.

## Key Features

1. **Exact and Relative Equality**: Detects both precise price matches and relative equality within a specified threshold.

2. **Customizable Appearance**: Allows users to adjust colors, line styles, and widths.

3. **Dynamic Line Management**: Automatically extends or removes lines based on ongoing price action.

4. **Labeling System**: Optional labels to identify types of equal levels (e.g., "Equal High", "REH/Equal High").

5. **Flexible Settings**: Adjustable parameters for lookback periods, maximum bars apart, and relative equality thresholds.

## User Inputs

### Appearance

- `lineColorHigh`: Color for lines marking equal highs (default: red)

- `lineColorLow`: Color for lines marking equal lows (default: green)

- `lineWidth`: Thickness of the lines (range: 1-5, default: 1)

- `lineStyle`: Style of the lines (options: Solid, Dash, Dotted)

- `showLabels`: Toggle to show or hide labels for equal highs and lows

### Settings

- `lookbackLength`: Number of bars to look back for finding equal highs and lows (default: 200)

- `maxBarsApart`: Maximum number of bars apart for equal highs/lows to be considered (range: 2-10, default: 5)

### Relative Equality

- `considerRelativeEquals`: Enable detection of relative equal highs and lows

- `thresholdIndex`: Maximum tick difference for relative equality in index instruments (range: 1-10, default: 2)

- `thresholdStocks`: Maximum tick difference for relative equality in stock instruments (range: 5-200, step: 5, default: 10)

## How It Works

The indicator scans historical price data to identify equal or relatively equal highs and lows. It draws lines connecting these levels and updates them as new price data comes in. Lines are extended if the level holds and removed if the price breaks through. The tool adapts to different market conditions by allowing adjustments to the equality thresholds for various instrument types.

## Practical Use

Traders can use this indicator to:

- Identify potential support and resistance levels

- Spot areas where price might react based on historical turning points

- Enhance their understanding of price structure and repetitive patterns

## Disclaimer

This indicator is provided as a tool to assist in identifying potential price levels of interest. It is not financial advice. Users should not rely solely on this or any single indicator for trading decisions. Always conduct thorough analysis, consider multiple factors, and be aware that past price behavior does not guarantee future results. All trading involves risk.

Mxwll Price Action Suite [Mxwll]Introducing the Mxwll Price Action Suite!

The Mxwll Price Action Suite is an all-in-one analysis indicator incorporating elements of SMC and also ideas extending beyond the trading methodology!

Features

Internal structures

External structures

Customizable Sensitivities

BoS/CHoCH

Order Blocks

HH/LH/LL/LH Areas

Rolling TF highs/lows

Rolling Volume Comparisons

Auto Fibs

And more!

The image above shows the indicator's market structure identification capabilities. Internal BoS and CHoCH structures in addition to overarching market structures are available with customizable sensitivities.

The image above shows the indicator identifying order blocks! Additionally, HH/LH/LL/LH areas are also identified.

The image above shows a rolling area of interest. These areas can be compared to supply/demand zones, where traders might consider a bargain long/short/sell area.

The indicator displays a rolling 4hr high/low and 1D high/low, alongside auto fibonacci levels with a customizable sensitivity.

Finally, the Mxwll Price Action Suite shows relevant session information.

Table information

Current Session

Countdown to session close

Next Session

Countdown to next session open

Rolling 4-Hr volume intensity

Rolling 24-Hr volume intensity

Introducing the Mxwll SMC Suite!

The Mxwll SMC Suite is an all-in-one analysis indicator incorporating elements of SMC and also ideas extending beyond the trading methodology!

Features

Internal structures

External structures

Customizable Sensitivities

BoS/CHoCH

Order Blocks

HH/LH/LL/LH Areas

Rolling TF highs/lows

Rolling Volume Comparisons

Auto Fibs

And more!

The image above shows the indicator's market structure identification capabilities. Internal BoS and CHoCH structures in addition to overarching market structures are available with customizable sensitivities.

The image above shows the indicator identifying order blocks! Additionally, HH/LH/LL/LH areas are also identified.

The image above shows a rolling area of interest. These areas can be compared to supply/demand zones, where traders might consider a bargain long/short/sell area.

The indicator displays a rolling 4hr high/low and 1D high/low, alongside auto fibonacci levels with a customizable sensitivity.

Finally, the Mxwll Price Action Suite shows relevant session information.

Table information

Current Session

Countdown to session close

Next Session

Countdown to next session open

Rolling 4-Hr volume intensity

Rolling 24-Hr volume intensity

Expanded Features of Mxwll Price Action Suite

Internal and External Structures

Internal Structures: These elements refer to the price formations and patterns that occur within a smaller scope or a specific trading session. The suite can detect intricate details like minor support/resistance levels or short-term trend reversals.

External Structures: These involve larger, more significant market patterns and trends spanning multiple sessions or time frames. This capability helps traders understand overarching market directions.

Customizable Sensitivities

Adjusting sensitivity settings allows users to tailor the indicator's responsiveness to market changes. Higher sensitivity can catch smaller fluctuations, while lower sensitivity might focus on more significant, reliable market moves.

Break of Structure (BoS) and Change of Character (CHoCH)

BoS: This feature identifies points where the price breaks a significant structure, potentially indicating a new trend or a trend reversal.

CHoCH: Detects subtle shifts in the market's behavior, which could suggest the early stages of a trend change before they become apparent to the broader market.

Order Blocks and Market Phases